When Your Insurance Company Suggests Medical Impossibilities

Disclaimers

- The following post is based entirely on my personal experience navigating the DC Government CareFirst BluePreferred PPO Plan and its Pharmacy Benefit Manager, CVS Caremark.

- I am a healthcare professional and a patient, not an attorney or an insurance broker. This is NOT legal or financial advice. While I make no guarantees about the results of using these methods, my goal is to share my knowledge, documentation strategies, and experiences so you can better advocate for your own health.

- This post is a direct follow-up to my previous guide on auditing your Explanation of Benefits (EOBs).

- Any information from conversations with CVS Caremark or CareFirst comes from my notes taken during the calls in my ‘patient’s log’ as described in my blog. These notes were taken contemporaneously to ensure an accurate, time-stamped record of the instructions provided to me. All references to contractual rights are drawn directly from the governing CareFirst Blue Preferred PPO Evidence of Coverage Document.

- Specific to the Certificate of Coverage (Evidence of Coverage), a CareFirst employee provided it to me when I was unable to obtain a copy from DCHR. If there is mismatch between the version I have and the version with DCHR, well that’s for another post. (Stay tuned.)

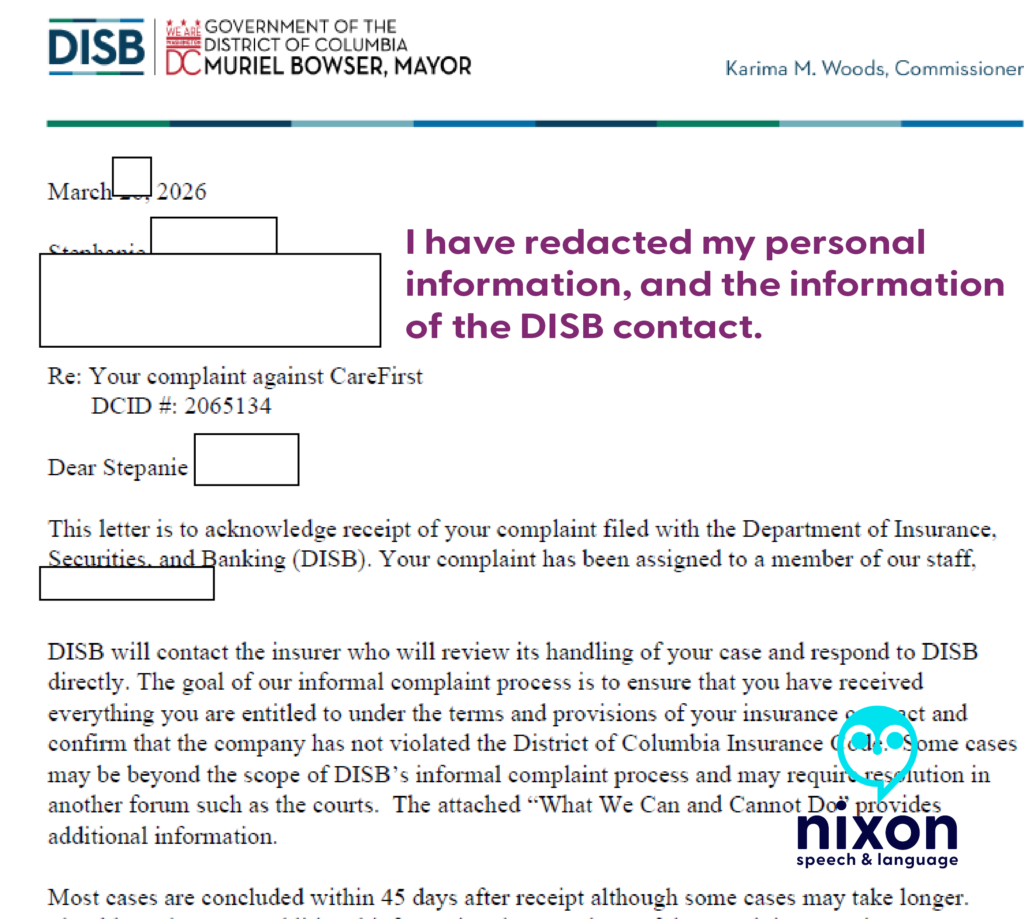

- Please note: I currently have a formal grievance regarding this matter under active review with the District of Columbia Department of Insurance, Securities & Banking (DISB; DCID#: 2065134). I have also contacted the DC City Council and Mayor’s office. All regulatory violations discussed below are alleged based on my documentation, and I will provide an update once I receive a final disposition.

The Tech Black Hole: Where Prior Authorizations Go To Die

If your doctor tells you they are waiting on your insurance, and your insurance tells you they are waiting on your doctor, someone is lying. Actually, it’s probably the software.

I tracked a pattern across five medical specialties (including neurology, gastroenterology, rheumatology, and my PCP). Providers were submitting prior authorizations through a vendor portal called CoverMyMeds. The system would tell the pharmacy the request was “sent,” but the providers never received the questionnaires. After 48 to 72 hours, the system automatically closed the files for “no response”.

This is a de facto denial of benefits without clinical review, likely caused by a software defect. I realized something was off in December 2025 when I was still with Aetna, but I thought it might just be the facility.

When providers had the same trouble in January 2026 with the same result, I realized that didn’t fit. It seemed more “systemic”, and the only commonality across these situations was that the prior authorizations were being submitted through CoverMyMeds. When speaking with a CVS Caremark Sr Rep in February, I was told that providers and patients had been expressing the same frustration I just noted. Additionally, you can see more here in the reviews.

(DISCLAIMER: This is an observation based on a pattern of incomplete PAs for the same reasons and the reactions of providers who all indicated the same issue: They never received requests for the information.)

Clinical Absurdity and Medical Impossibility

What do you do when a senior representative at your Pharmacy Benefit Manager (PBM) suggests you ask your provider to give a 30-day prescription for a 90-day quantity of a medication?

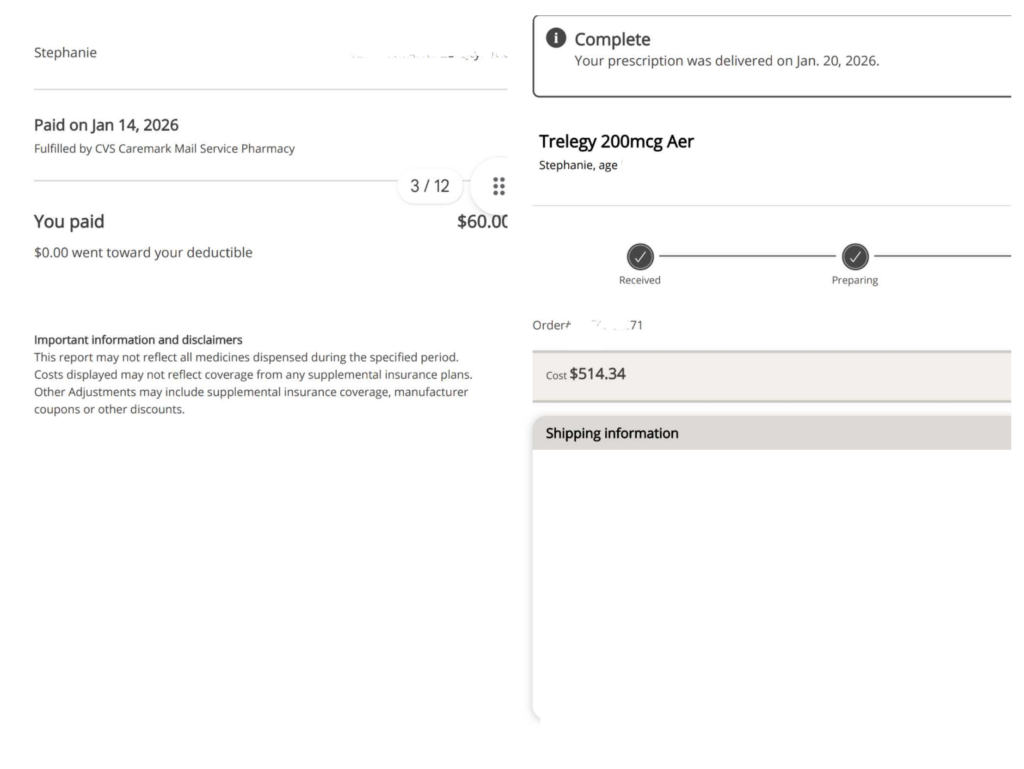

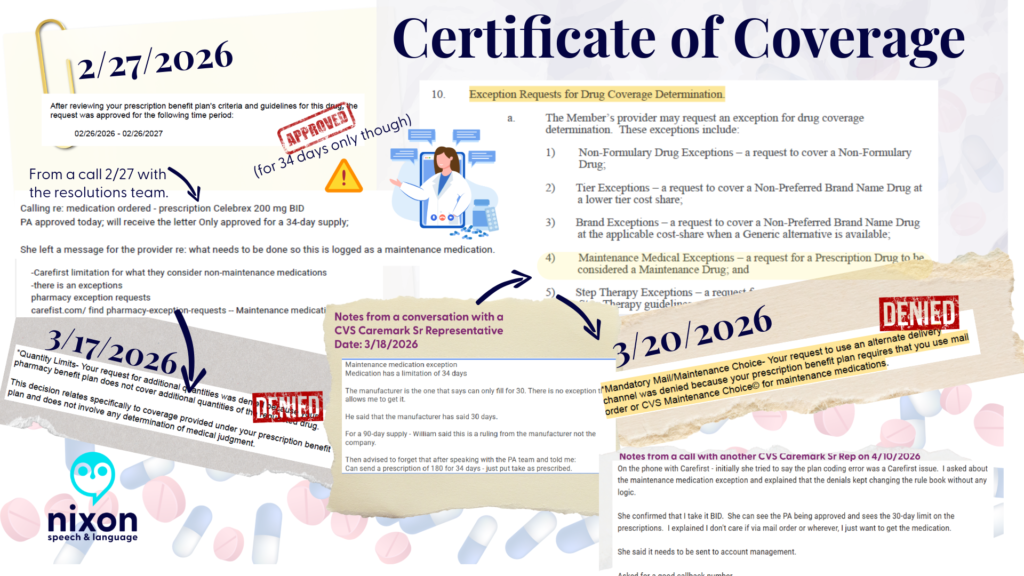

I’ve been taking the same dose of a brand-name maintenance medication for over 20 years. Recently, my PBM, CVS Caremark, approved my brand medically necessary PA (2/27/2026) but restricted the system to only dispense a 34-day supply. (This changed to 30-days less than 12 days later.)

What followed was a masterclass in administrative gaslighting:

- Excuse 1: First, they told me I just needed my provider to file a ‘maintenance exception’.

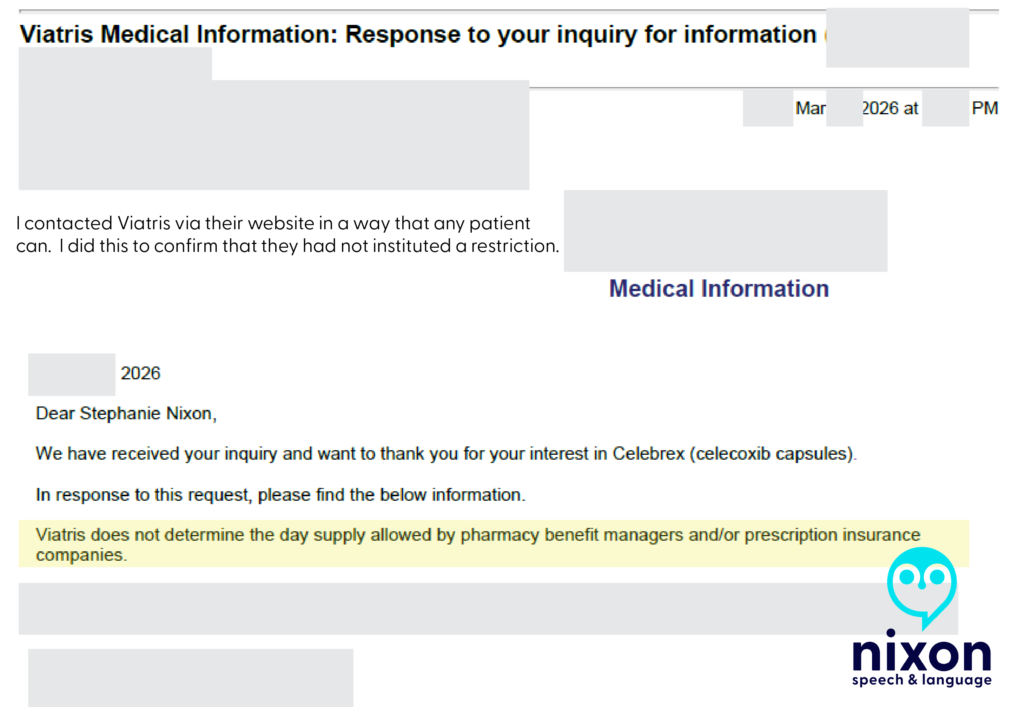

- Excuse 2: Then, they told my provider that an exception didn’t actually exist. When I called CVS Caremark, a Senior Representative blamed the manufacturer, claiming they restrict the medication to 30 days. I addressed this odd statement as there is nothing on the manufacture’s website or the web indicating the recommendation was accurate*.

- The “Solution”: Finally, the Senior Representative spoke with the Prior Authorization team again. Their solution? Have my provider submit a prescription for 180 Celebrex 200 mg capsules to be taken over 30 days.

* Note. That is 6 pills a day of a medication where the FDA safe limit is two. Also, while on hold on that date, I emailed the manufacturer, Viatris, and received the response below:

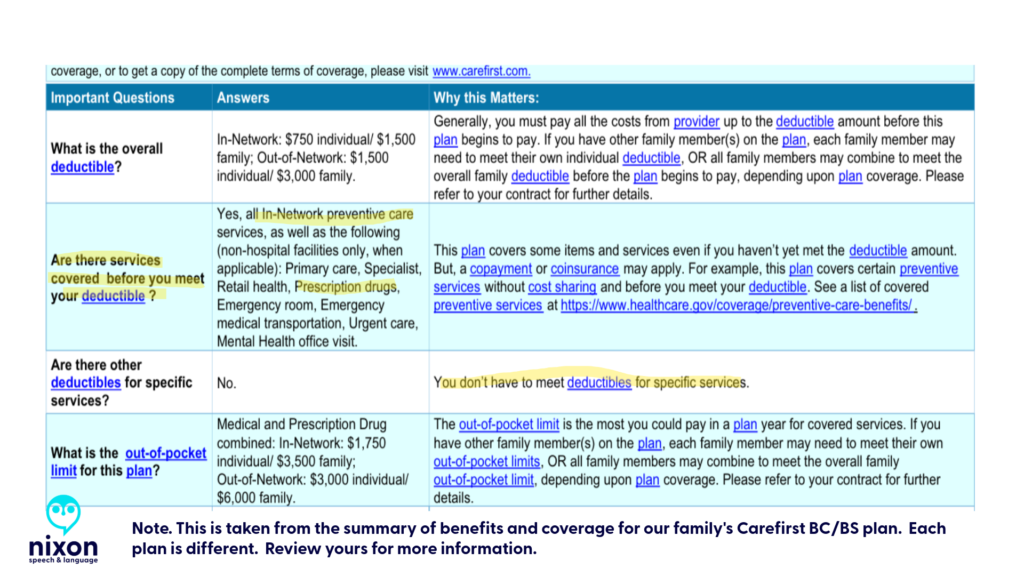

-CareFirst BluePreferred PPO Certificate of Coverage (Plan Sponsor: Government of the District of Columbia) (Obtained via CareFirst)

-Responses to medication PA requests from CVS Caremark

-Notes from my conversations with representatives at CVS Caremark

I was stunned. I pointed out that this sounded like “creative pharmaceutical benefits”—otherwise known as insurance fraud. The representative laughed.

I didn’t know what to say as I got off the phone.

I spoke with my amazing Health Advocate and PCP, and then dug into my hundred-page policy myself.

I found Section 10(a)(4), which explicitly allows a medication like mine to be classified under a “Maintenance Medical Exception” for a 90-day fill. So I’m unsure what rules the senior representative was looking at, but they definitely did not match the rulebook the CVS Caremark Resolutions Specialist saw on 2/27/2026.

So, I filed a complaint with DISB

DISB is the District of Columbia Department of Insurance, Securities, and Banking.

Since that date, I have contacted DC City Council and Mayor Muriel Bowser via email. There are more issues than just the above, but I will explain how I did this in another post.

As of 4/10/2026

After an almost 1-hour call with CVS Caremark on 4/10/2026, a Senior Representative informed me that she could see the maintenance medication exception in my plan documents. At the end of the call, she said that the issue needed to be sent to “account management” and that such issues are often corrected after 5 business days.

I have not heard anything as of 4/18/2026.

The Patient’s Playbook: Protect Yourself

Insurance companies rely on your exhaustion. You must document everything and demand your legal rights.

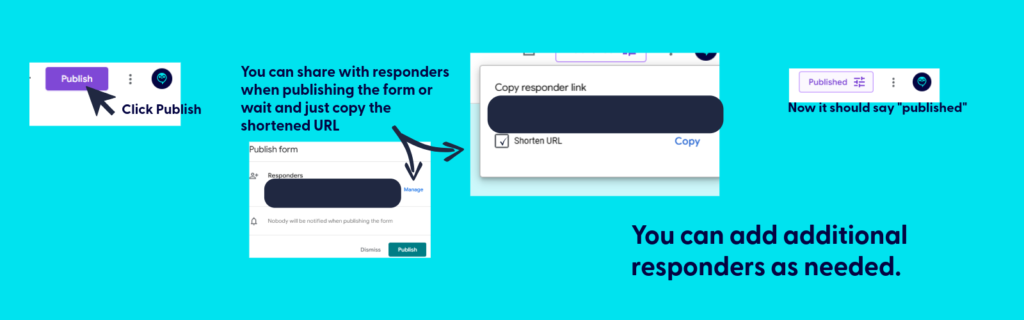

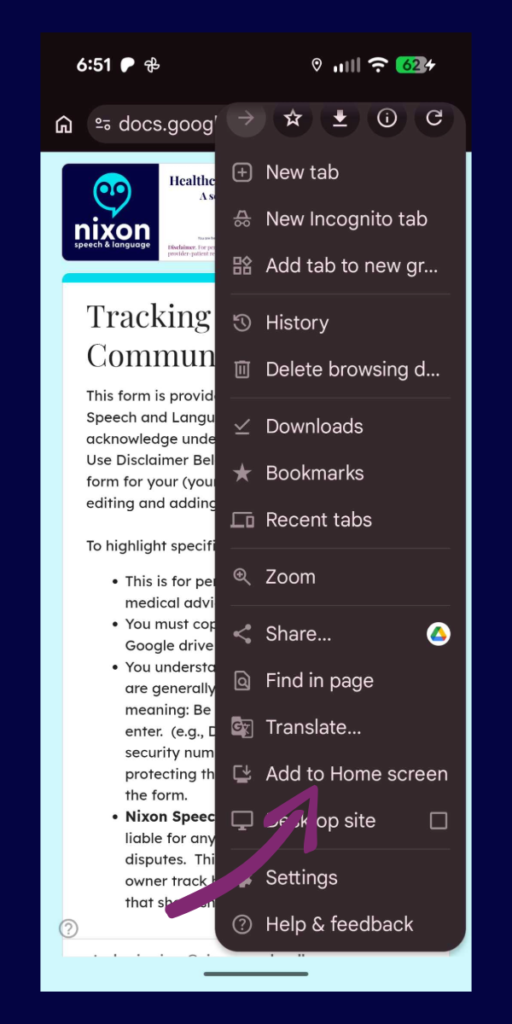

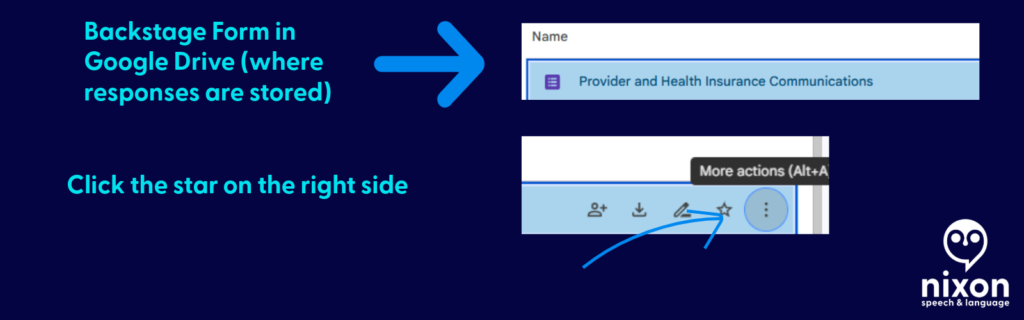

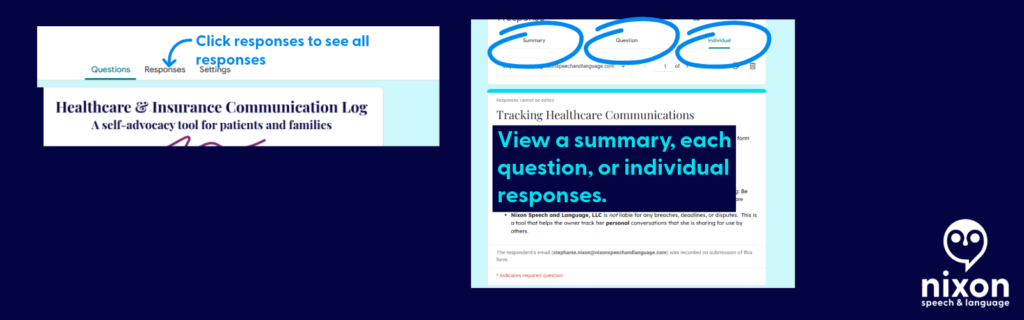

- Track Every Call: Stop scribbling on scrap paper. Use the free Google Form I created—my “Patient’s Log”—to track the date, time, representative name, and action items of every call. Evidence is the only thing that wins appeals.

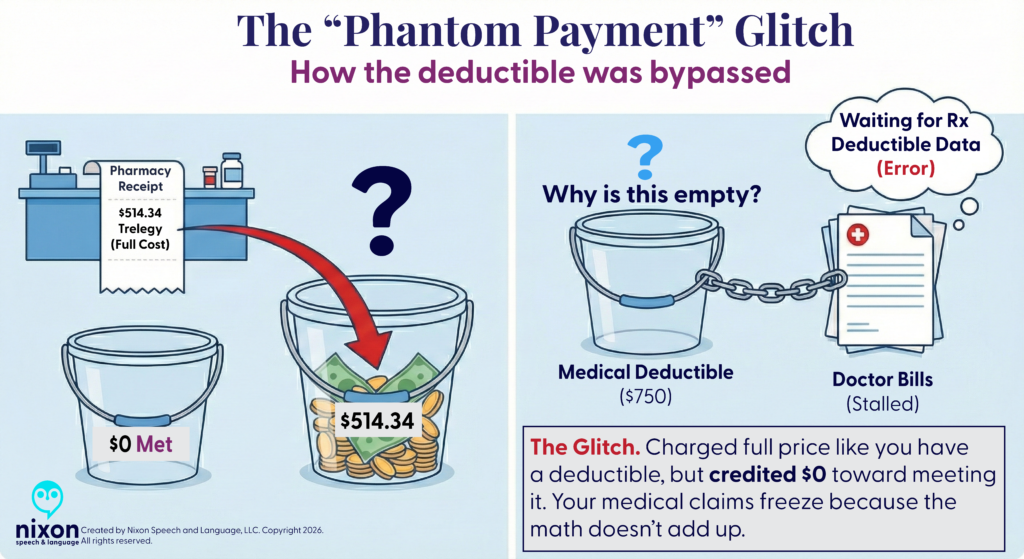

- Check Your EOBs: If you are on a PPO and see a sudden deductible applied to standard pharmacy claims, call your insurer, demand an “Accumulator Adjustment,” and report a “Plan Design Error.”

Never take a verbal denial at face value. You must read the actual rules in your Certificate of Coverage (COC) to catch their lies—just like a Resolutions Specialist pointed out the ‘Maintenance Medical Exception’ in my contract leading me to push a Senior Representative at CareFirst about the frustration I had actually…getting one. (i.e., I couldn’t.)

The Golden Rule: Get Your Certificate of Coverage (COC)

Patients and Providers: Never take a verbal denial at face value. Demand the policy in writing, contact the manufacturer if they are blamed, and report “creative pharmaceutical benefits” to your state insurance administration immediately

To do this, you must get a copy of your Certificate of Coverage (COC). This is the governing rulebook—usually over 100 pages—not the short “Summary of Benefits.”

Under federal disclosure standards (specifically ERISA), if you submit a written request to your plan administrator for your governing plan documents, they are legally required to provide them to you within 30 days. Failure to comply with this federal disclosure window can carry potential statutory penalties of up to $110 per day.

Stay tuned—because simply obtaining my COC from the DC Government (DCHR) has been an entirely separate battle. I have a copy, but not via DCHR, despite repeated requests.

🗣️ Please share this post and tag @MayorBowser, @CMCHenderson, and the DC City Council Committee on Business and Economic Development. We need proactive DISB market conduct audits, not just individual complaint responses.

Trademarks and Fair Use Notice: All company names, logos, and trademarks—including CareFirst BlueCross BlueShield, CVS Caremark, Viatris, and any brand-name prescription drugs (such as Celebrex)—are the property of their respective owners. Their inclusion in this post and associated images is for educational, informational, and advocacy purposes only and does not imply any affiliation or endorsement.

Copyright © 2026 Nixon Speech and Language, All Rights Reserved.

- Google Health’s: The Master of Context and Your Early Warning System

- Words Have Weight: The “Saga” of Subjective Charting

- Words Have Weight: Stopping the ‘Deranged Twitter Feed’¹ in Your Chart

- Words have Weight: Labels vs. Life, Part 1a

- Words have Weight: The Mirror Test, Part 1b

Access and advocacy Bias chronic illness claims processing clinical documentation bias Clinician Associated Patient Trauma communication log deductible Department of Education doge Dyslexia education empower patients errors processing claims google health Guava Health Health apps healthcare communication disparities health insurance health insurance appeals health insurance mistakes Independent Funding innovation Institute of Education Sciences invisible illness Kanban Task Tracker managing your health max out of pocket medical gaslighting examples medical record transparency medicolegal risk more than labs neurodivergence NIH Organizer patient advocacy in healthcare patient gaslightling pharmacy benefit managers Planner providers Research Funding Spoonie life subjective vs. objective medical notes wearable technology Words have Weight

Access and advocacy, health insurance, health insurance mistakes, pharmacy benefit managers